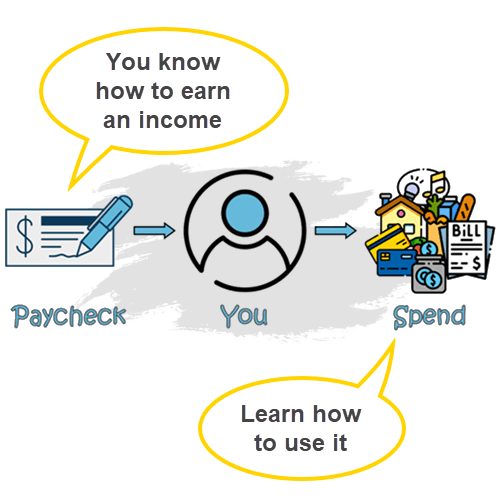

The linchpin of the paycheck to paycheck lifestyle is payday. Paychecks are also the focus of traditional budgeting, tracking expenses and keeping a spreadsheet. This seems to make obvious sense since payday is when we get more money. But therein lies the basic reason that we get in trouble with our everyday money: we’re looking at our everyday money in the wrong direction.

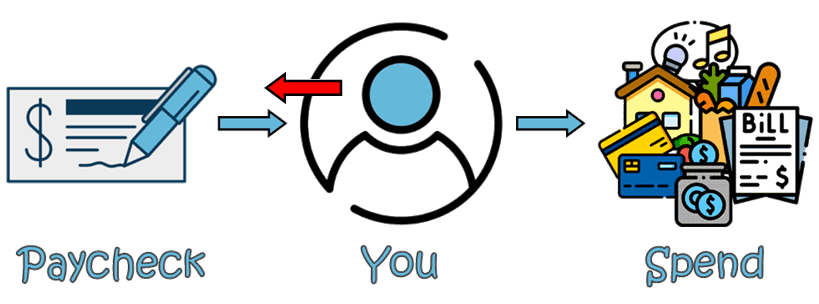

Our default view of our income is backward toward paychecks as indicated below by the red arrow. Focusing on paydays, however, puts our view of our money in direct opposition to the direction that our everyday money flows, as shown by the blue arrows.

The problem with looking backward to paydays is that there is no standard schedule for paychecks. Whoever is issuing the checks decides when payday happens. On the other hand, when we need our money is on schedules that are recognized and adhered to world-wide: bill and credit card payments come due on some type of monthly schedule.

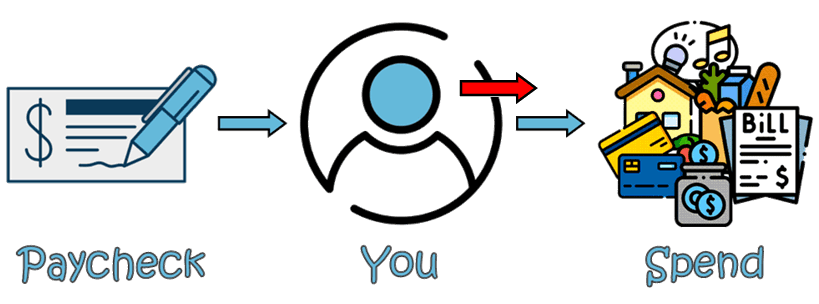

The basic fix for our money troubles, therefore, appears to start with changing our view of our everyday money from when we get paychecks to when we need to make payments, as shown below.

With paydays and payment due dates on very different schedules, how can we coordinate what’s coming in with what’s going out? Actually, that is easy to do with a checking account.

By replacing “You” with a checking account we disconnect the inflow of cash from the outflow. By depositing all of our paychecks, in full, into a checking account, we create a money reservoir that functions just like a dam on a river.

The water behind a dam accumulates from the natural flow of the river. When the water is released from the reservoir is determined by when the outflow is needed to produce power. Inflow is separate from outflow as long as outflow does not exceed inflow.

We can give ourselves the same fundamental control of our everyday money by routing our paychecks through one checking account. We can plan our spending based solely on when the money is needed. This is more natural than trying to micromanage paychecks. It also makes something else possible that’s been missing: a standard way to view and manage everyday money that is flexible enough to work for everyone. A method that is free from the tyranny of paydays and living paycheck to paycheck.